Key Points:

- The current consensus estimated corporate earnings for the Malaysia equity market are expected to grow by 12.6% and 14.5% in 2011 and 2012.

- Based on market capitalisation, sectors that represent around 69% and 75% of the FBMKLCI are expected to post double-digit earnings growth in 2011 and 2012 respectively.

- However, with the potential of a slowdown in global economy growth, there is increasing risk that the estimated earnings might be slashed.

- If we revise downward the estimated earnings for 2011 and 2012 by 5% and 7% respectively from the current level, earnings growth is therefore expected to be lower at 7.0% and 12.1% in 2011 and 2012.

- Regardless of this, we remain to see record earnings over the next two years.

- The forward PE based on current estimated earnings and downward revised estimated earnings remain lower than the historical level of 16x, indicating that the Malaysia equity market is still undervalued.

- Both earnings estimation approaches are expected to provide an upside potential of 26.6% and 17.8% by end of 2012.

- Recommended Fund For Malaysia: Kenanga Growth Fund, Areca EquityTRUST Fund

Selling Pressure Emerged As Investors Become More Cautious

As at 11 August 2011, the Malaysia equity market, which represented by the FBMKLCI index, slumped by 3.1% from 1524.43 points (5 August 2011). Investor’s sentiment has weakened due to the resurfacing of double-dip recession fear, while at the same time, the European debt crisis has reduced investor’s risk appetite. Most of the equity markets, including Malaysia, resume their decline after a short-rally on 10 August, where the Federal Reserve promised to keep interest rates low through mid-2013.

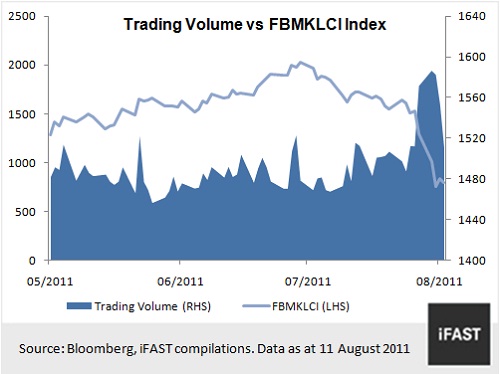

Trading volume in Bursa Malaysia has surged since 5 August, with the FBMKLCI moving downward since then (refer to Chart 1). This indicates that selling pressure emerged as investors become more cautious due to the current market volatility.

Will Corporate Earnings Be Slashed?

We always stress to investors the importance of corporate earnings as the ultimate factor that drives the equity market over the long-term. The current consensus estimated corporate earnings for the Malaysia equity market are expected to grow by 12.6% and 14.5% in 2011 and 2012 (data as at 11 August 2011), mainly supported by the banking sector that have a weightage of about 35% in the FBMKLCI. Other index heavy-weighted sectors such as Telecommunications, Gaming, Plantation, as well as Construction sectors are also expected to post double-digit earnings growth in 2011 and/or 2012 (refer to Table 1). Based on market capitalisation, sectors that represent around 69% and 75% of the FBMKLCI are expected to post double-digit earnings growth in 2011 and 2012 respectively.

Sector Weightage in FBMKLCI (%) 2011 2012

| Banks 35.2 13.1% 13.7% |

Holding Companies 10.3 14.2% 12.0%

(Diverse)

Plantation 8.3 10.2% 5.7%

Gaming 8.0 25.9% 11.4%

Chemicals 4.2 11.3% 30.1%

Oil and Gas 3.8 5.5% 6.4%

Construction 1.4 48.2% 14.6%

Auto Manufacturers 1.3 37.3% 13.8%

Total 87.5 - -

Source: Bloomberg, iFAST compilations. Data as at 11 August 2011

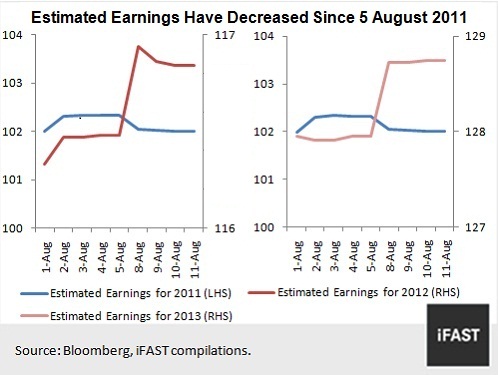

However, with the potential of a slowdown in global economy growth, there is increasing risk that the estimated earnings might be slashed. In fact, consensus data shows that the estimated earnings for 2011 have gradually decreased since 7 August 2011, while earnings for 2012 and 2013 have increased since then (refer to Chart 2). We expect the upcoming quarterly reporting season, which will begin by the 3rd week of August, to serve as a critical factor in determining the adjustment to estimated earnings.

Chart 2

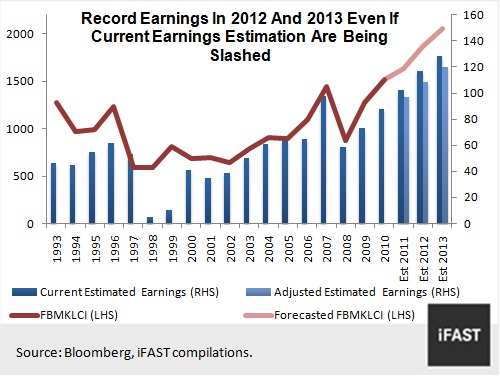

If we assume the estimated earnings for 2011 and 2012 are revised downward by 5% and 7% respectively from the current level, earnings growth is therefore expected to be lower at 7.0% and 12.1% in 2011 and 2012, as compared to the current estimation stated above. Regardless of this, we remain to see record earnings over the next two years (refer to Chart 3).

CHART 3:

Valuations Look Attractive

The Malaysia equity market is currently traded at forward PE of 14.6x and 12.6x based on estimated earnings for 2011 and 2012 (data as at 11 August 2011). If we take a more conservative approach by using the downward revised estimated earnings, the forward PE is estimated to be 15.2x and 13.6x. The forward PE for both approaches remain lower than the historical level of 16x, indicating that the Malaysia equity market is still undervalued.

In addition, with a fair PE of 16x, the current estimated earnings as well as the downward revised estimated earnings are expected to provide an upside potential of 26.6% and 17.8% by end of 2012. This should be decent returns for investors who are willing to undergo the current market volatility. Investors who wish to have exposure in the Malaysia equity market may consider our recommended funds, the Kenanga Growth Fund and Areca equityTRUST Fund (www.fundsupermart.com.m)

No comments:

Post a Comment